Demand is the power to purchase a product coupled with willingness to purchase it. If a consumer holds only one of them, then the meaning of demand does not hold. Take the case of a poor man; he may be willing to purchase expensive goods. But his willingness is not supported by the ability to purchase i.e. the necessary money.

On the other hand, a rich man may afford to buy an expensive car, say a Jaguar. However, he is not willing to do so because he knows that its maintenance is quite expensive. Therefore, he refrains from purchasing that car, even though he has the ability to purchase.

See Also: Economics is a Science as Well as an Art

What is Law of Demand | Different Definitions

The law of demand is a fundamental principle in economics that describes the relationship between the price of a good or service and the quantity demanded by consumers. It states that, all else being equal, as the price of a product increases, the quantity demanded for that product decreases, and vice versa. This law reflects the basic behavioral pattern of consumers in the marketplace.

Here are different definitions of the law of demand as provided by various authors:

- Alfred Marshall stated the law of demand as, “When the price of a commodity increases, the quantity demanded for it decreases, and when the price of a commodity decreases, the quantity demanded for it increases, other things being equal.”

- James Tobin defined the law of demand by saying, “The response of quantity demanded to a change in price, with other influences on demand held constant, is negative.”

- According to Paul A. Samuelson: “The law of demand states that, other things being equal, when the price of a good rises, the quantity demanded of that good falls, and when the price falls, the quantity demanded rises.”

- Gregory Mankiw defines the law of demand as, “The law of demand states that, all else being equal, when the price of a good rises, the quantity demanded of that good falls.”

These definitions all express the same fundamental economic law, which is the inverse relationship between price and quantity demanded. When the price of a product rises, consumers typically buy less of it, and when the price falls, they tend to buy more, assuming that all other factors that affect demand remain constant.

Principles of the Law of Demand

The Law of Demand is a fundamental concept in economics that explains the relationship between the price of a good or service and the quantity demanded by consumers. It is based on several key principles that help us understand how changes in price affect consumer behavior. Here are few of them.

-

Inverse Relationship Between Price and Quantity Demanded:

At the core of the Law of Demand is the idea that, all else being equal (ceteris paribus), there is an inverse relationship between the price of a product and the quantity demanded by consumers. This means that as the price of a good or service increases, the quantity demanded decreases, and vice versa.

In simpler terms, when prices go up, people tend to buy less of a product, and when prices go down, they tend to buy more. This principle is commonly depicted as a negatively sloping demand curve on a graph.

-

Diminishing Marginal Utility:

One of the underlying reasons for the inverse relationship is the concept of diminishing marginal utility. This principle states that as consumers consume more of a particular product, the additional satisfaction or utility derived from each additional unit decreases.

When the price of a product is high, consumers will purchase fewer units because the marginal utility of each additional unit is lower. As the price drops, consumers find the product more attractive, and they buy more units because the marginal utility per unit increases.

-

Ceteris Paribus (All Else Being Equal):

The Law of Demand assumes that all other factors affecting demand remain constant, a concept known as “ceteris paribus.” In the real world, many factors influence consumer demand, such as income, consumer preferences, the prices of related goods, and more. To isolate the impact of price changes, economists use this assumption to simplify analysis.

-

Consumer Rationality:

The Law of Demand also assumes that consumers are rational decision-makers. They aim to maximize their utility by allocating their income to purchase goods and services in a way that provides the greatest satisfaction.

Rational consumers respond to price changes by adjusting their purchasing decisions. When a product’s price falls, they may buy more of it because it becomes a better value.

-

Demand Curves:

To visually represent the Law of Demand, economists use demand curves. These curves show the relationship between price and quantity demanded. The demand curve typically slopes downward from left to right, illustrating the inverse relationship between price and quantity.

-

Elasticity of Demand:

Elasticity of demand is a measure of how responsive quantity demanded is to changes in price. Elastic demand indicates that consumers are highly responsive to price changes, while inelastic demand suggests they are less responsive. The Law of Demand often operates differently depending on whether the demand for a good is elastic or inelastic.

These key principles help us understand how consumers react to price changes, which is essential for businesses, policymakers, and economists in making informed decisions about pricing, production, and market behavior. While the Law of Demand is a simplified model, it provides a valuable framework for analyzing consumer choices and market dynamics.

Factors Affecting Demand

Factors affecting demand are essential to understanding how consumer behavior changes in response to various influences. Demand, in economic terms, refers to the quantity of a good or service that consumers are willing and able to buy at various prices during a specific period. The following are key factors that influence demand:

-

Price of the Product:

The most significant factor influencing demand is the price of the product itself. According to the Law of Demand, as the price of a product increases, the quantity demanded tends to decrease, and vice versa, assuming all other factors remains constant (ceteris paribus). This price-quantity relationship is typically illustrated on a demand curve.

-

Consumer Income:

Normal Goods: For most goods, as consumer income increases, demand increases. These goods are referred to as normal goods. For example, when people earn more money, they are likely to spend more on vacations, dining out, and other luxury items.

Inferior Goods: In contrast, for inferior goods, as income increases, demand decreases. Inferior goods are those for which people buy less of when they have more income. For example, used cars or generic food products may be considered inferior goods.

-

Consumer Preferences and Tastes:

Consumer preferences, influenced by various factors such as advertising, trends, and cultural shifts, play a significant role in shaping demand. Products that align with current consumer preferences tend to experience higher demand.

-

Price of Related Goods:

Substitute Goods: When the price of a substitute product (a product that can replace another) increases, demand for the original product may increase. For example, if the price of coffee raises significantly, the demand for tea, a substitute for coffee, may increase.

Complementary Goods: Complementary goods are consumed together. When the price of one complementary good increases, demand for the other may decrease. For example, if the price of smartphones increases, the demand for smartphone cases, a complementary good, may decrease.

-

Consumer Expectations:

Consumer expectations about future prices, incomes, and economic conditions can influence current demand. If consumers expect the price of a product to increase in the future, they may buy more of it now. Conversely, if they expect future incomes to decrease, they might reduce their current consumption.

-

Population and Demographics:

The size and demographics of a population can significantly impact demand. Growing populations or changes in demographics (e.g., aging populations, increased immigration) can lead to shifts in demand for various goods and services.

-

Advertising and Consumer Awareness:

Effective advertising campaigns can create consumer awareness and increase demand for a product. Well-executed marketing strategies, brand recognition, and positive consumer perceptions can drive demand.

-

Government Policies:

Government policies such as taxes, subsidies, and regulations can affect demand. For instance, tax incentives for electric vehicles can increase demand for such vehicles. Conversely, regulations that restrict the sale of certain products (e.g., tobacco) can decrease demand.

-

Seasonal and Weather Factors:

Seasonal changes and weather conditions can influence demand for specific products. For instance, demand for winter clothing increases in cold weather, while demand for ice cream rises during the summer.

-

Cultural and Social Influences:

Cultural and social factors can impact demand, especially for products with cultural or social significance. For example, demand for certain foods or beverages may be influenced by cultural or religious celebrations.

Understanding these factors is crucial for businesses, policymakers, and economists when making decisions regarding pricing, production, marketing, and other aspects of managing the supply and demand for goods and services in the market.

Law of Demand Graph and Table

The law of demand is a fundamental concept in economics, stating that all else being equal, as the price of a good or service decreases, the quantity demanded for that good or service increases, and vice versa. This relationship is often depicted graphically using a demand curve. Here’s a detailed explanation of the law of demand with a graphical representation:

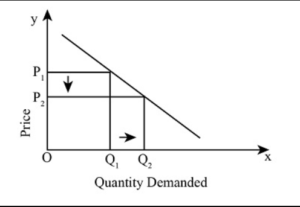

The Demand Curve: The demand curve is a graphical representation of the law of demand. It shows the relationship between the price of a product and the quantity demanded by consumers. In a typical demand curve:

- The vertical axis (Y-axis) represents the price of the product.

- The horizontal axis (X-axis) represents the quantity of the product demanded.

Slope of the Demand Curve: The law of demand is illustrated by the downward slope of the demand curve. As the price decreases (moving from left to right along the X-axis), the quantity demanded increases (moving up along the Y-axis), and as the price increases, the quantity demanded decreases.

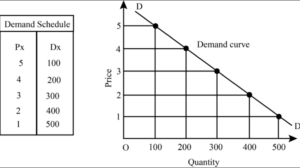

Demand Schedule: To create a demand curve, you start with a demand schedule. A demand schedule is a table that lists various prices and the corresponding quantity demanded at each price point. Here’s a simplified example of a demand schedule for a hypothetical product:

| Price (in $) | Quantity Demanded |

|---|---|

| 1 | 100 |

| 2 | 200 |

| 3 | 300 |

| 4 | 400 |

| 5 | 500 |

Demand Curve Construction: Using the demand schedule, you can create a demand curve. For our example, the demand curve would be downward-sloping, as shown in the graph below:

The left side of the graph represents a higher price ($5) and a lower quantity demanded (100 units).

The right side of the graph represents a lower price ($1) and a higher quantity demanded (500 units).

Interpretation: This graph illustrates the law of demand. As the price of the product decreases, from $5 to $1, the quantity demanded increases. Consumers are willing to purchase more of the product when it is cheaper.

Understanding the law of demand and its graphical representation is essential in economics, as it provides insights into how consumers react to price changes, and it is a fundamental concept in market analysis and decision-making.

Slope of the Demand Curve

In economics, this is known as the negative slope of the demand curve. The reason according to the law of demand is, as price goes up quantity demanded goes down and vice-versa. As the position of the slope in both ways is slanting, it seems to be negative.

Negatively Sloped Curve Factors

-

Price Effect

Due to a fall in the price of a product, it invites more consumers to purchase more of that product. Therefore, the quantity of that product in the market goes up.

-

Income Effect

When the price of good goes down, automatically income of the consumers, seems to have gone up, thus enabling them to purchase more of the product.

-

Substitution Effect

When the price of good ‘A’ goes down, the price of good ‘B seems expensive relative to. Therefore, the consumer shifts the money he normally spends on good ‘B’ and prefers buying good.

Here, substitution is taking place. Take the example of beef and mutton. When the price of mutton goes down, Ahmad purchases more mutton than beef.

Remember the price of beef remains the same but seems expensive to Ahmad because the price of mutton has gone down from its original price.

Ahmad’s income is unchanged. He substituted some of the money previously used for purchasing beef so as to buy more mutton, suppose, in the beginning, the price of both the commodities was $40 per Kg. The price of mutton went down to $30 per Kg. Therefore, Ahmad substituted $0 from his beef expenditure, for mutton.

Assumptions of Law of Demand

-

Income Remains Constant

The income of the consumer must remain constant for the law of demand to hold. If there is a change in his income.

The result will not be regarded in accordance with the law of demand e.g. if the income of the consumer falls and the price of the good remains constant’ the consumer will purchase less of the good though its price does not increase. It is so as there is a fall in his power.

-

Habits And Fashions should not Change

The consumer must not develop a sudden disliking for the product he usually purchases, even though there is a fall in its price. He must not also become suddenly eager to add to the consumption of that product. In short, the consumer must remain rational.

-

Price of Related Goods should Remain Constant

Whether a given change in the price of a related goodwill increase or decrease, the demand for the product in question will depend on whether the related good is a substitute for or a complement to it.

Butter and margarine are substitutes. A rise in the price of butter leads the consumers to more margarine. Hence, demand for margarine increases. Petrol cars are complements. Consumptions Of petrol increases with a decrease in the price of cars and thus an increase in the demand for oil.

-

No Change in Future Circumstances

The consumer must not consider possible future changes in purchasing products, e.g.

If he feels that in the future the price of good A will rise substantially, he purchases a lot now to stock up in spite of the fact that the price has not changed.

-

Weather and Population should Remain Constant

During the winter season, the utility of woolen clothes goes up, even though they might be very expensive. Whereas changes in demand due to changes in population are concerned, we can say that utility of milk rises due to an increase in the number of consumers even though the price of milk is constant.

-

Disregarding New Substitutes

The consumer must not change to different/new products, e.g. the consumer is accustomed to a cloth of quality A. However, when cloth is being selected by her, she prefers to purchase cloth type B, even though there is no change in tie price of cloth type A. Hence, this condition is an assumption.

Exceptions of Law of Demand

As we know that Demand is the power to purchase a product coupled with a willingness to purchase it. There are several assumptions of law of demand, but there are also certain exceptions of law of demand. These exceptions of law of demand are discussed below: –

-

Very High-Priced Products

Diamonds, luxurious cars etc are demanded by wealthy people. Even though their prices may go up there will still be a demand for them. Furthermore, the prices of these goods generally do not fall.

-

Very Low-Priced Products (Inferior Goods)

In the case of inferior goods e.g. salt, even though its price may fall, the demand for it will not rise. This is so because people will not start consuming salt in large quantities with a fall in its price.

-

Ignorance of the Consumer

Often the consumer is not unduly bothered about the price he is paying, even though it is possible that he may be able to pay less for the same good in another shop.

He does not go to other shop merely because he is not aware of its lower Prices, in such cases the law is not applicable.

-

Increase in Marginal Utility of the Consumer

Say a purchase an everyday for given price. If on a particular day he needs the newspaper for important information any other special reason.

His marginal utility will rise, even though is paying the same for it. But according to the law of demand, marginal utility should always equal to price.

Change in Demand

There are two types of changes in demand.

- Extension and contraction of demand.

- Rise and fall of demand

-

Extension and Contraction of Demand

Extension and contraction demand occurs due change in the price of the respective commodities. Extension means that there is increase in the quantity of the purchased due to a fall in its price. Contraction means that there a m of the good due to the rise in its price.

-

Rise and Fall of Demand

The law of demand states that price and quantity demanded move in the opposite direction. i.e. when the price rises, the quantity demanded falls down.

However, there are times when there is a rise in demand even though the price remains the same or goes up. Whereas as the law of demand states that when the rice goes up the quantity demanded falls down hence, there is a rise in demand here.

Causes of Change in Demand

-

Changes Income

As the income of the consumer rises, he will purchase more products which are still available at the same prices. Hence their demand will arise and vice-versa when his income decreases.

-

Changes in Taste and Fashion

If a certain commodity is out of style or fashion, the demand for it will decrease even though its price has not changed.

For example, few years back, we had the “bell-bottoms” trend and the demand for them was high during that particular period; but it has now gone down.

Another example concerns new competitive when these are available in the market for the same prices as the old products. They will increase for the former and decrease for the latter. So, there will be a change in demand due to change in Fashion.

-

Changes in Weather

During the summer season, the demand for tea or coffee is consumers prefer soft drinks. However, during the winter season. There will be a rise in demand for tea and coffee, even though their prices may remain constant throughout the year.

-

Changes Population

It will be a rise in demand for such as milk, clothing, etc. due to an increase in the number of consumers, as the population increases, because more consumers will now enter into the market.

-

Changes in the Quantity of Money

This usually occurs when the government has a budget deficit, i.e. government expenditure exceeds its revenue and government prints more money to cover up the deficit. In such a situation, generally, the prices of consumer good rise which later on lead to fluctuation in demand for them.

-

Change in Distribution of Income

A typical society usually comprises two main classes in the community; the lower-class, and upper-class; and there is unequal distribution of income. In a capitalist society, this leads to increase hardships and suffering for poor and a fall in the for the products takes place.

However, if there is a fair distribution of income, this will put the lower-class at about the level as the upper class. The result would be that the lower-class consumers would like to consume more products. Hence there will be a rise in demand.

-

Rate of Economic Growth

When the rate-of economic growth there is an increased production of goods and services, hence a rise in demand and vice-versa.

-

Discovery of a Substitute

When this happens, naturally there is a desire to tie product. This leads to a rise in the demand for the new product even though prices of both the old and new products are almost the same.

For example, earlier people used coal as their main means of heating/burning something. But when gas was discovered the utility of coal went down.

-

Changes in the Prices of Substitutes

Consumer in a community usually consur1E about the same amount of beef and mutton. However, if the price of mutton goes up and that of beef remains constant, demand will fall for mutton and rise for beef.

-

Change of Taste

Change of taste can affect demand, too e.g. people used to consume 2-3 teaspoons full of sugar when taking their tea or coffee. Whereas now a days people consume only I-1\2 teaspoons full sugar. The demand for sugar was high earlier but now there has been a fall in demand for it.

Law of Demand |Graph | Table | Assumptions | Exceptions | Change in Demand | PDF Free Download |

Conclusion

The law of demand is a fundamental concept in economics that reflects how consumers react to changes in prices. It is a crucial principle for understanding consumer behavior and market dynamics. When prices rise, consumers typically buy less, and when prices fall, they buy more of a product, assuming other factors remain constant.